Met Money 3

Met Money 3

Is it time to question the "best practices" of the watchdogs?

Just a quick introductory note: this one might be shorter than I will normally be gunning for. I’m going to prioritize trying to get something out on Friday or Saturday each week, but sometimes regular work intervenes! So, be prepared for a 3.1 or 3.2 here. And don’t worry, I won’t always be talking about this topic (though don’t bother me about NFTs).

In Met Money 1 I challenged arguments for the billionaires on The Met’s board to “save” the institution from its $150 million shortfall, which the museum has proposed to fund through sales from its collections. In Met Money 2 I took to task the main tenets of the “slippery slope” argument that any sales from The Met’s collection to fund anything other than buying more for that collection would be the end of The Met as we know it — and the end of many other museums too, which would inevitably follow The Met’s lead down its well-intended path to hell (or so the slippery slopers believe).

I trust that after reading those pieces you will at least join me in retiring any use of the word “operations” on its own to indicate staff salaries at museums. I know this may seem like a minor point, but when considering the policy documents of organizations, be they the museums themselves or the “watchdogs” (as Thomas Campbell put it) such as the Association of Art Museum Directors (AAMD), the language and the terminology matters.

The debate over The Met’s proposal to sell some portion of its collections to fund the salaries of its staff would never have been a debate at all had the AAMD not opened the doors to the action by “relaxing” its regular prohibitions on selling art for purposes other than acquisitions. On April 15 of last year, the AAMD issued a statement that the organization would “refrain” from using its regular suite of punishments — “censure, suspension and/or expulsion” for the director; “censure and/or sanctions” for the institution — against any museum that “decides to use restricted endowment funds, trusts, or donations for general operating expenses.” The AAMD in this context should be lauded, as it explicitly states that the use of these funds for “operations” includes “necessary” expenses such as “staff compensation and benefits.”

It’s only in the context of “collections” that AAMD continues to take a hard line on how funds raised from sales might be used. According to the April 15 resolution, “An institution may use the proceeds from deaccessioned works of art to support the direct care of the museum’s collection,” and that,

This temporary approach is not intended to incentivize deaccessioning or the sale of art, only to provide additional flexibility on the use of the proceeds from art that may be sold. AAMD’s longstanding principle that the proceeds from deaccessioned art may not be used for general operating expenses remains in place.

As the AAMD notes, its resolution “effectively places a moratorium on punitive actions through April 10, 2022,” which means the doors that it was opening to The Met’s and others’ proposals would close after two years (but more on this in a moment).

There is a lot to unpack here. From the standpoint of The Met’s proposal, the essential concept to understand — and debate — is “direct care” of a collection: what is it? what constitutes it? and importantly, are collections staff — conservators, registrars, handlers, etc. — included in the concept? The answer to these questions is: It’s up to the institution! The museum’s collections policy delineates what’s included in direct care, and the board of any museum can decide on what’s in and what’s not. The AAMD, and the American Association of Museums (AAM), and the Federal Accounting Standards Board (the FASB) are all in agreement on this point.

As is The Met, for that matter. Max Hollein’s statement in response to The Met’s early vocal critics is very careful to demonstrate that what The Met is proposing is perfectly in line with both the spirit and the letter of the AAMD’s regulations. It just comes down to how one wants to define “direct care,” and in that case, again, it’s up to the institution itself.

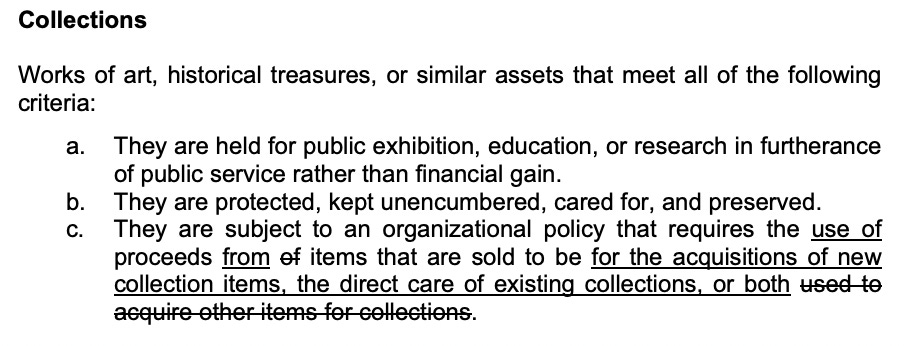

It’s worth noting as well that this “direct care” consideration is a relatively new one. The FASB only recently updated its own guidance on how collections of “works of art, historical treasures, and similar assets” are (or are not) recognized as such. The 1993 Statement 116, to which AAMD makes direct reference in its 2011 policy handbook, explicitly states that one of the conditions for non-recognition of assets is that they enter a collection that is “subject to an organizational policy that requires the proceeds from sales of collection items to be used to acquire other items for collections” (no, we’re not talking great literature here). In 2019, this condition was updated to reflect the Code of Ethics published by the AAM.

It is only in the last decade then that the “direct care” line has been opened up to museums, and it’s worth noting that in this, the FASB and thus the generally accepted accounting practices (GAAP) that govern how most museums account for their assets (or don’t) is being directed not by the FASB, which would give museums plenty of cover, but by the museums themselves, and in this case the American Alliance of Museums.

So the AAMD’s April 15 resolution, at least as it regards the sales of works of art from the collection to pay salaries, provided they are connected to collection care, should not have an end date. Why would it? That action is sanctioned by the AAM and has been recognized by the FASB since 2019.

All of which suggests, to me at least, that a bold board, and a willing museum director, could expand the definition of “direct care” to include, oh, I don’t know, let’s say… museum security? What else are The Met’s security staff for if not the direct care and protection of the collections in the galleries. Every stern shake of the head or remonstrance for the flash of an iPhone going off is a contribution to the direct care of the collections, and of the ones that matter most to the public, one might argue, given that they are the only ones to which the public has access.

In fact, one could imagine writing a policy in which the concept of “direct care” could be expanded to include the full operational activity of the museum — that is, all of the people that contribute to the educational mission of the institution and thus generate a community that actual does care (if now even indirectly) about the stuff in the collections, but who also only very likely care about the stuff in the collection because there is a hard-working and often underpaid museum staff (and volunteers!) who actually give a shit — I mean who care about the institution and the collection and the public being served.

What I mean to say is that while “direct care” on the face of it seems to make sense — museum collections are getting bigger, and older, and demand more resources and expertise to keep them up — when you dig down into it, it’s difficult to understand where “direct care” of the collection ends and the rest of the museum begins. Sure, parking doesn’t seem to be entailed in the direct care of the collections — but recall that parking is a big revenue generator for museums (especially here in Los Angeles) and those funds go in some part to the pool of funds out of which museum salaries and wages are paid. If even one dollar of parking revenue can be shown to pay the wage of a museum guard, then why would one argue against parking as a means to care for the museum’s collection?

Yes, I understand it’s a stretch, but the closer one looks at the AAMD carve out, as well as the deaccessioning policies and the web of accounting rules and amendments in which they are caught up, the more one gets the sense that a great deal of effort (and bureaucracy) is being put to ensuring that a strict hierarchy is maintained between the two most integral components of any art museum — the things and the people. And the things are always coming out on top — to the extent that the people who really do care about and for those things are paying for those things (and those institutions) with their jobs.

The GAAP of the FASB are very clear about one thing, however:

Current GAAP also states that [a not-for-profit] that holds works of art, historical treasures, and similar items that meet the definition of a collection has the following three alternative policies for reporting that collection: capitalization, capitalization of all collection items on a prospective basis (that is, all items acquired after a stated date), and no capitalization.

Even though the AAMD looks to the FASB for some of its authority on these matters, it’s clear that the FASB is neutral on the question of collections as assets, and even offers two-to-one options on how to, in my opinion, make better use of them. To capitalize, or not to capitalize, would seem to be the question.

In light of all the layoffs and furloughs, AAMD’s policy pronouncements on the financial status of their members’ collections — such as “The collections the museum holds in public trust are not financial assets and may not be converted to cash for operating or capital needs,” or “To present fairly the museum’s financial position, collections should not be capitalized,” or “Member museums should not capitalize or collateralize collections or recognize as revenue the value of donated works” — look not a little bit mean.

As always, thank you for reading. You can get these drafts direct to your inbox by subscribing. And please feel free to share and to comment.